News

How to Save Estate & Gift Taxes with Grantor Trusts: The Basics

The United States imposes the estate tax for the privilege of passing assets to your beneficiaries after you die and the gift tax for transfers during life. The tax rates on transfers are among the highest in the world, with a top rate of 40%. While estate taxes are only applied to estates larger than $5.45 million (in 2016), this amount includes every asset that you own including your residence, real estate, 401(k), stocks, bonds, closely-held companies, cash, cars and even the death benefits of your life insurance. For many, the size of their estate for tax purposes may surprise them.

The United States imposes the estate tax for the privilege of passing assets to your beneficiaries after you die and the gift tax for transfers during life. The tax rates on transfers are among the highest in the world, with a top rate of 40%. While estate taxes are only applied to estates larger than $5.45 million (in 2016), this amount includes every asset that you own including your residence, real estate, 401(k), stocks, bonds, closely-held companies, cash, cars and even the death benefits of your life insurance. For many, the size of their estate for tax purposes may surprise them.

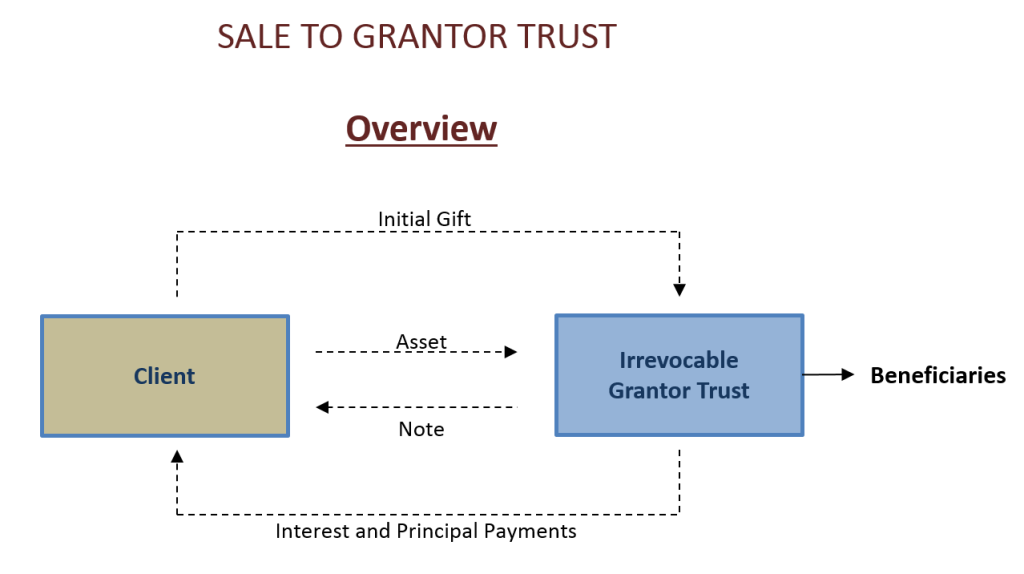

One of the most effective estate planning techniques used to minimize federal transfer taxes is the installment sale to a grantor trust. This technique essentially removes appreciating property from your estate and is replaced by a long term promissory note. This technique is one of many which “freeze” the value of an asset for purposes of estate, gift or generation skipping transfer taxes (collectively, these taxes are often referred to as “transfer taxes”). By freezing the value, future appreciation grows outside of your estate, thereby escaping transfer taxes, possibly for multiple generations.

Grantor Trust

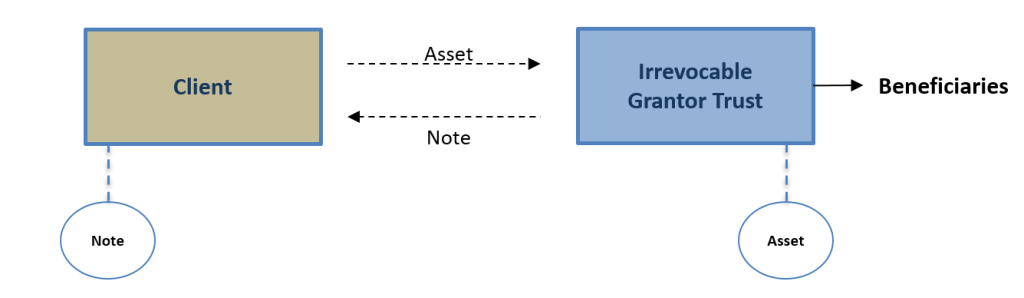

The key element of this technique is the establishment of the grantor trust. A grantor trust is an irrevocable trust, which owns the assets held by it for transfer tax and state law purposes, but the assets are treated as owned by the individual grantor for income tax purposes. This differing treatment is allowed because the definition of a completed transfer in the income tax section of the Internal Revenue Code (“IRC”) is different than the transfer tax section of the IRC. As a result, the sale of an asset by a grantor to a grantor trust is ignored for income tax purposes because it is treated as a sale from the grantor to himself or herself — in other words, it is a non-event and no gain or loss is recognized. If the asset is sold in exchange for a promissory note, the interest paid by the trust to the grantor is also not recognized and no income is recognized by the grantor. The trust, however, is not ignored for transfer tax purposes. If an asset is gifted to the trust, the transfer would be subject to gift taxes. If the asset is sold for full and adequate consideration, the transfer would not be subject to gift taxes as it is not a gift. Full and adequate consideration can be in the form of a promissory note as long as the principal amount of the note reflects the fair market value of the asset sold and the interest rate payable on the note is not less than the “applicable federal rate.” This rate is published monthly by the IRS and varies based on the length of the note’s term.

Upon the grantor’s death, the value of the assets held by the trust should not be included in the grantor’s estate. Instead, only the balance of the promissory note will be subject to estate taxes, thereby shifting all appreciation following the date of the sale out of the grantor’s estate.

Structuring the Plan

Description of the sale transaction seems simple enough. However, as the saying goes, the devil is in the details. There are many aspects to this technique that must be carefully considered. Once in place, the ongoing administration of the technique is just as important as the structure and also must not be overlooked.

(1) Establish the grantor trust: A grantor trust will replicate, in large measure, the grantor’s will or revocable trust. After all, the trust is to provide for the disposition of assets of the trust after the grantor’s death. Unlike a revocable trust, the grantor typically is not the trustee of the grantor trust. An irrevocable trust is considered a “grantor trust” if the grantor retains certain control or rights over the assets, where the grantor or trustee has the ability to benefit the grantor directly or indirectly. A planner can intentionally “trigger” the grantor trust status by drafting the trust agreement to include these powers such as (i) by giving the grantor the power to reacquire trust property by substituting asses of equivalent value, and (ii) by giving the trustee the power to make a loan to the grantor without adequate interest or security.

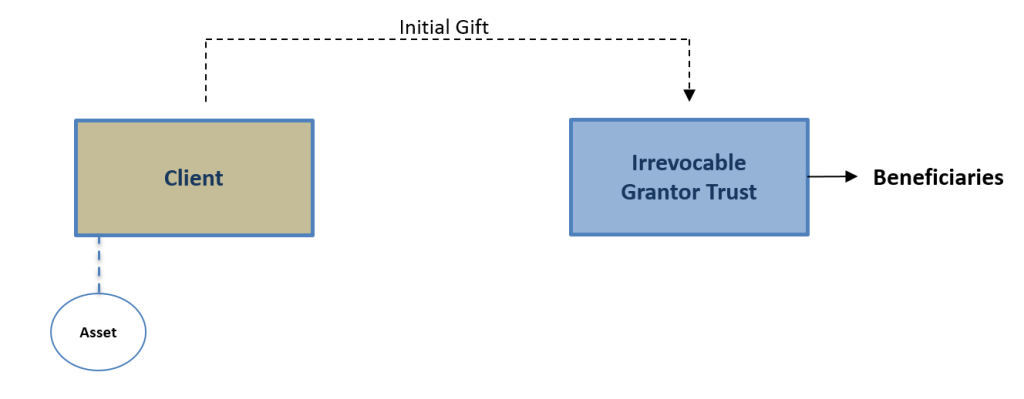

(2) Initial funding of the trust: Once the trust is established, it is generally recommended to make an initial gift to the trust. The purpose of this transfer is to get the trust capitalization in addition to the assets purchased with the promissory to provide additional security for the loan. This capitalization can be in the form of cash or other assets. Although a common recommendation is make a gift equal to at least 10% of the purchase price for the assets the grantor intends to sell to the trust, many commentators consider lower percentages acceptable. Higher percentages are considered conservative. The transfer of the initial funding will be in the form of a gift, which will likely be subject to gift taxes. In lieu of making this initial gift, some practitioners recommend the use of personal guarantees of the promissory note by beneficiaries.

(3) Sale Documentation: Although the sale to the grantor trust is ignored for income tax purposes, the sale is intended is to be respected for all other purposes including property law purposes. Therefore, the sale should be structured as a sale to an unrelated third-party, and the documentation should be prepared accordingly. Typical documentation will include a purchase agreement, assignment, promissory note, and security agreements as necessary.

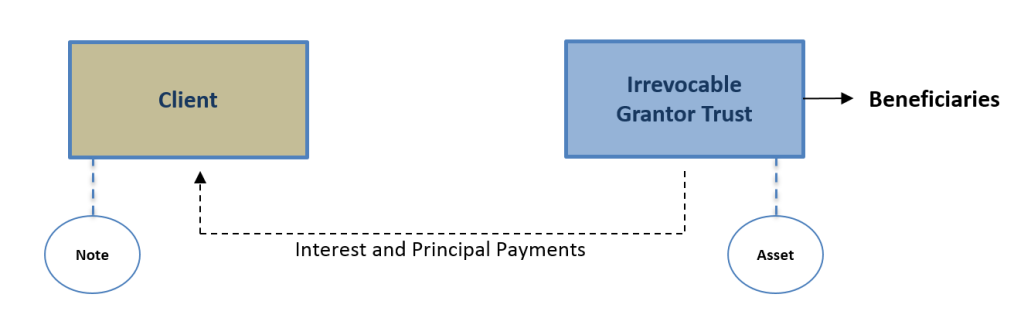

(4) Promissory Note Payments of Interest and Principal: As mentioned earlier, the promissory note must bear interest at a minimum equal to the rates prescribed monthly by the IRS. Promissory notes can be structured with terms ranging from short-term (demand notes) to long-term notes, typically not to exceed the life expectancy of the grantor. The note can be fully amortized over the term of the note or it can be interest-only, or any variation in between. The effectiveness of the freeze technique is maximized by keeping payments as low as possible. Therefore, the interest-only note is very common, and, typically, the prepayment of principal is allowed by the trustee to provide a greater cash flow if desired. The payments on the note should be made from the initial gift made to the trust or the cash flow generated by the assets held by the trust. If necessary, in-kind payments can be made from the trust assets back to the grantor when cash is not available to satisfy the note payment. Upon the maturity of the note, any outstanding principal must be repaid to the grantor or the grantor’s estate.

Income Tax Treatment

The grantor trust is treated as the grantor for income tax purposes. Therefore, the sale from the grantor to the grantor trust is a nonrecognition event and does not trigger any gains or losses. The same is true with the interest payments from the grantor trust to the grantor. As such, interest payments are not treated as income to the grantor. Any income or losses generated by the trust assets will be considered received by the grantor and reported on the grantor’s personal return. The grantor trust can be created to allow the trustee to reimburse the grantor for taxes the grantor paid in connection with the trust assets.

Gift Tax Treatment

Any transfer to the grantor trust will be subject to gift taxes unless consideration of equal value is received by the grantor in return. The funding of a grantor trust with the initial gift typically will be a taxable gift, but most often sheltered by the lifetime exclusion amount. It is very important that the sale of assets to the trust must be for fair market value. Otherwise, any undervaluation could allow the IRS to argue that the transfer was a part gift, thereby exposing the transfer to additional estate or gift taxes.

Estate Tax Treatment

The value of an asset that is sold to a trust will not be included in the grantor’s estate for purposes of calculating the estate tax. However, the payments received from the trust plus any outstanding principal owed on the promissory note will be included in the grantor’s estate. This technique removes appreciating property from the grantor’s estate but adds the non-appreciating note to the grantor’s estate. The estate and gift tax savings result if the assets held by the trust have a total net return (i.e., income and capital appreciation) that exceeds the interest rate on the note. The greater appreciation of the property, the greater the potential benefit of this technique.

Example

Annie has a substantial estate and wishes to transfer shares of her closely-held company to her grantor trust. The trust is initially funded with a gift of $500,000, and later the shares of the company with a fair market value of $5 million are sold to the trust in exchange for a promissory note with a 10 year term. Seven years later, Annie’s company triples in value and is sold to a strategic purchaser. The grantor trust sells its share of the company for $15 million. However, the outstanding principal on the promissory note to Annie remains at $5 million. The difference between the value of the trust assets at the end of the note’s term and the amount of assets paid back to Annie during the course of the note escapes transfer taxes. In this case, Annie was able to transfer approximately $10 million to the beneficiaries of the grantor trust without paying gift or estate taxes on such amount.

Conclusion

A sale to a grantor trust is a powerful estate planning tool that can reduce estate and gift taxes and pass substantial wealth to future generations. It is ideal for income generating assets as well as assets with large potential appreciation (such as speculative real estate and investments in start-up companies).