News

Appealing Ad Valorem Tax Assessments

Elizabeth J. Daniels, Caitlein J. Jammo, and Eric J. Brooks

Administrative and judicial challenges to property tax assessments in Florida are governed by relatively short and strictly enforced deadlines. Around the state, Value Adjustment Boards (“VAB”) are convening, and VAB hearings will continue through the end of the year.

Administrative and judicial challenges to property tax assessments in Florida are governed by relatively short and strictly enforced deadlines. Around the state, Value Adjustment Boards (“VAB”) are convening, and VAB hearings will continue through the end of the year.

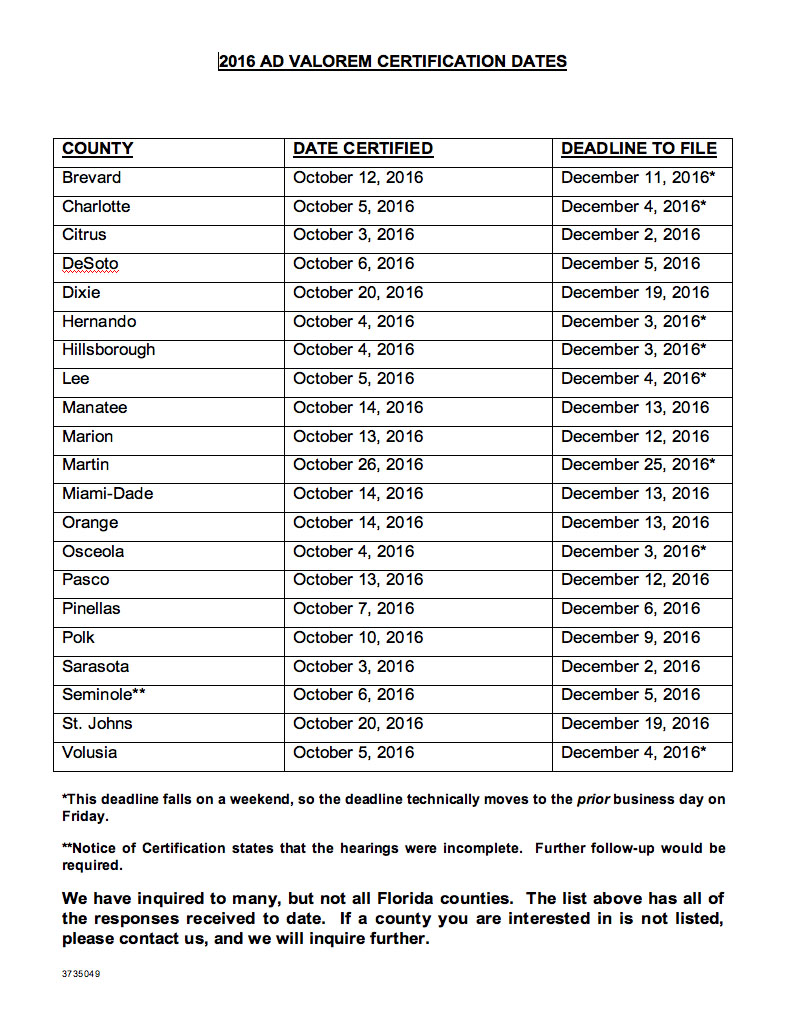

Those taxpayers who wish to appeal their assessment—but either did not submit a petition to their county’s VAB or did petition the VAB but are dissatisfied with the result—must file an action in their local circuit court within 60 days of the date of the property appraiser’s initial certification of the tax rolls. Failure to file within the 60-day period will be an absolute bar to an appeal of that year’s tax assessment. We have compiled the initial certification dates and appeal deadlines for Bay Area and Central Florida counties here. In the counties we surveyed, those deadlines begin as early as December 2, 2016.

For those taxpayers who timely filed a VAB petition, judicial appeals must be filed within 60 days of the date the VAB renders its decision on their petition (not from the date of mailing or receipt of the board’s decision).

Before bringing a court action to appeal a tax assessment, the taxpayer must pay at least a good faith estimate of the taxes owed. A taxpayer also must make a good faith payment of taxes before delinquency where VAB proceedings are still pending.1 A VAB petition is not a prerequisite to filing a circuit court case, but at this point deadlines for any 2016 assessment appeal would be extremely close. Payment of the taxes or of a good faith estimate does not prejudice a taxpayer’s right to timely challenge the tax assessment.

The information provided above represents only the most basic rules governing your appeal. Property tax challenges are subject to an extensive number of constantly changing rules and statutes. Accordingly, it is always best to check promptly with a knowledgeable attorney when there are any unique facts for a particular property or appeal.

_________________________

1 §194.014, Fl. Stat. This fairly new provision has caused difficulties for many owners and tax reps and should be carefully monitored by anyone with a pending VAB proceeding that might ultimately want to file suit.